Small enterprises can get funds through business loan options other than the conventional banking system. Business loans include things like online loan marketplaces, crowdsourcing websites, third-party payment processors like PayPal, and cryptocurrencies like bitcoin.

For the majority of enterprises, Business loans entails submitting an online loan application. Fintech lenders are another name for these lenders that combine the words “finance” and “technology.” The majority of fintech lenders employ various techniques for establishing eligibility, and they are often designed to tolerate a different amount of risk than banks.

Be aware that some business funding options, such as term loans and credit lines, are available from both conventional (bank-based) and alternative (internet-based) lenders.

Alternative VS Conventional Business Financing

While there are many other types of alternative business loans, which is a sizable segment, the traditional business financing market is more constrained. Term loans and credit lines from a bank or credit union are examples of traditional business financing.

As compared to alternative business loans, banks are far less likely to grant your request for funding for a business, and major banks are less likely to do so than small banks. Banks have stricter borrower requirements because they are less risk-averse than other lenders. For instance, you might just need one year of business experience to get approved for a loan from an internet lender, but you’ll need at least two years to secure a loan from a bank. Another difference between traditional and alternative business loans is that it’s hard to get traditional loans online. Usually, you have to go to your bank to fill out an application.

A traditional business loan often has a lower interest rate and a longer payback period than an alternative business loan, although it is more challenging to get. This is because alternative lenders sometimes charge more for the extra risk they take when giving money to new small businesses.

17 Types of Business Loans For Small Businesses

These are best types of business loans for business startup in UK.

#1. Lines of Credit

website: https://www.loc-online.co.uk/

A line of credit (LOC) is a sort of business financing that you may obtain from both a bank and an internet lender, but, just like term loans, business LOCs are sometimes easier to obtain online than through a bank. If you’re not familiar with the concept, a line of credit is essentially a quantity of money that you are given permission to withdraw from whenever you need it. It can serve as a source of working capital for a business or a financial safety net (much like a credit card). You only pay interest on the money you borrow.

A useful alternative to a business loan option for a business that doesn’t need a precise sum of money but needs access to additional capital to meet costs (like payroll) during tough times is an online business line of credit.

#2. Online Loans

website: https://www.paydayuk.co.uk/

Online lenders offer business financing solutions such as term loans and credit lines that are comparable to those provided by banks. Online loans, however, vary from bank loans in a few key respects. Online loans often have fewer restrictions on your credit score, length of business, and yearly income. Additionally, they need less time to fund and are simpler to qualify for. There is only one restriction: online loans often have higher interest rates and costs than bank loans in return for this accessibility and convenience.

Short-term loan (STL) providers online, in particular, have exceptionally lenient conditions and exorbitant interest rates. (Our article on short-term business loans is a useful primer on the subject.)

#3. Term Loans

website: https://www.everyday-loans.co.uk/long-term-loans

Historically, a term loan, also known as an “instalment loan,” was taken out by a business from a bank or credit union. The term “term loan” simply means that the loan is repaid over a predetermined period of time with a fixed or variable interest rate (for example, six months or five years). In actuality, this sums up the design of the majority of conventional business loans. There is a brand-new species of term loan available online, though.

You can apply for a term loan through the website of an online lender, a loan marketplace, or even a website for crowdsourcing (more on that later).

#4. Merchant Cash Advances

website: https://www.gov.uk/business-finance-support/merchant-cash-advance-uk

Despite not being loans, merchant cash advances (MCAs) have a comparable function. Your future profits are advanced through merchant cash advances. A lender advances you a predetermined amount of money and then begins collecting the money by withholding a portion of your daily credit card profits. This implies that your daily payment will vary according to your sales. The MCA business will keep taking a portion of your daily sales until they are paid back, which usually doesn’t happen in a set amount of time.

Unless you are ineligible for any other loan product, I would generally advise against getting an MCA because they are considerably more costly and possibly predatory than STLs. But MCAs are one of the few ways that new businesses, businesses with bad credit, and other struggling businesses that can’t get regular loans can get money.

#5. Personal Loans

website: https://www.hsbc.co.uk/loans/products/personal/

Obtaining a typical business loan might be challenging if your company is new and you don’t currently have significant income. Fortunately, a lot of personal loans can be used for business needs as well. Your family’s income and personal creditworthiness decide your eligibility for these loans, which are often structured as regular instalment loans, as well as the interest rates.

You might anticipate having access to less money with this kind of funding. Most personal lenders have $35K or $50K loan limits. If you need more money than this, you should not get a personal loan.

#6. Business Credit Cards

When paying for business costs without getting a loan, using business credit cards might be helpful. They allow you to purchase expensive or inexpensive things while receiving incentives and establishing your business’s credit profile. It’s a good idea to keep a business credit card on hand for when you need it, even if you don’t absolutely need to make a significant purchase right now.

Make sure to select a business credit card that offers you the greatest cash back (or miles, or other incentives) for the kinds of transactions your business makes the most regularly. For instance, some business cards are perfect for charging business trip expenses, while others offer rewards for regular office costs like electricity and office supply purchases. Some cards also have introductory APRs that are 0% for the first year.

#7. Microloans

website: https://www.microloanfoundation.org.uk/

Microloans are low-interest small business loans with a maximum amount of $35K (usually closer to $5K-$10K). Microloans are typically granted to start-ups or young companies in need of working capital. They frequently assist underrepresented or disadvantaged groups, including people with poor credit, by providing loans to enterprises run by women, veterans, and people of colour.

Banks haven’t been very interested in giving out loans for such small amounts of money in the past, but recently, both for-profit and non-profit alternative lenders have started giving out microloans.

#8. Sba Loans

website: https://www.gov.uk/apply-start-up-loan

Small Business Administration (SBA) loans, which are guaranteed by the US government, are a great alternative to traditional bank loans and, in certain situations, may be obtained through an internet lender. The SBA does not provide loans; rather, it backs a portion of loans made by banks, credit unions, nonprofit organisations, and other lenders. The guarantee states that in the event of your loan’s failure, the SBA will pay back a portion of the outstanding balance. As a result, the bank is able to cut the interest rate it would otherwise charge you.

The general 7(a) small business loan is the most well-known of the SBA’s loan programs.After approval, receiving SBA loan cash might take up to several months. However, some online lenders employ technology to streamline and speed up the SBA loan application process, so you might obtain your loan several weeks sooner.

Most SBA loans require two years of business experience, strong credit, a 10% down payment on the principle, and some kind of collateral in order to be approved.

#9. Invoice factoring

The financing method of invoice factoring releases funds from unpaid invoices. This is how it goes: Your unpaid invoice will be purchased by the invoice factoring business, or “factor,” who will normally advance you 85–95 percent of the invoice’s value. The factor then obtains payment from your client and delivers you the balance of the invoice, less a factoring charge of 1 to 5 percent. The length of time it takes your customer to pay is one element that affects your factoring cost.

As you may anticipate, invoice factoring is suitable for companies that regularly have unpaid bills and, as a result, have cash flow issues. Even though there may be a significant factoring charge involved, it may be worthwhile if you want quick cash, particularly if you dislike finding and collecting from past-due clients. Bad credit is usually not a problem because the main considerations are your customer’s capacity to pay and not your company’s. Because of this, younger companies and startups are eligible for this alternate financing option.

#10. Invoice financing

website: https://www.british-business-bank.co.uk/finance-hub/invoice-finance/

Although the two names have a similar sound, invoice financing and invoice factoring are distinct. With invoice financing, your unpaid invoices serve as collateral for a line of credit that the finance business gives to you. The amount of your unpaid invoices determines how big the line of credit will be. Since the financing business does not actually buy the bills, you are still responsible for getting payment from your clients. (Remember that with invoice factoring, you sell your invoices for quick cash, and the onus of collecting payments on those bills shifts to the factoring provider.)

For companies with outstanding bills but no imminent need for cash or any issues with a third party collecting from their clients, invoice finance is a wise option. Generally speaking, invoice financing has lower costs than invoice factoring.

#11. Equipment financing

Financing for equipment is precisely what it says it is. The equipment you need to run your business, whether it is a new computer system or industry-specific gear, is therefore money you borrow.

Loans and leases are both included in the definition of “equipment finance.” The greatest candidates for equipment loans are businesses that can afford a down payment on long-term useful equipment. If you can’t afford a down payment or if the equipment has to be changed or improved regularly, leasing is a better option.

#12. Business expansion loans

It covers the expense of relocating to a new location or expanding a current one. This enables development and expansion to be more easily afforded. Loans for business development are exactly what they sound like: money to help you pay for growing your business. This type of financing can be used to buy new property or a franchise, set up a new website, hire new employees, buy resources and equipment, or buy a new car.

The majority of loans are created with growth in mind. Several large banks provide business loans in order to help small firms pay for whatever they need to expand. Private loan providers can provide a wide range of loan options for business growth.

monetary examples

- Santander-Borrow between £2,000 and £25,000 for a period of 1 to 5 years, with fixed monthly payments.

- Borrow from $1,000 to more than $100,000 with Barclay’s.

- 365 Business Finance offers merchant cash advances from £5,000 to £200,000.

#13. Trade, Import & Export finance

website: https://www.british-business-bank.co.uk/export-finance/

An important yet challenging objective for many firms is to trade globally. Trade, import, and export financing can help businesses thrive by covering the initial costs of imports and export. Working capital, credit insurance, and bond support are examples of this sort of financing.

UK Export Finance is a service offered by the government to help companies get contracts overseas, make upfront purchases, and protect themselves in case a buyer backs out.

monetary examples

- UK Export Finance: Financing to help businesses effectively export their products.

- Touch Financial provides financing to support worldwide business success.

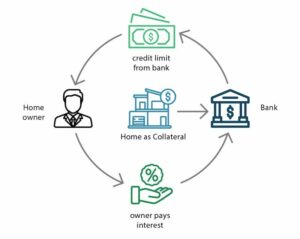

#14. Unsecured vs Secured loans

website: https://www.hsbc.co.uk/

Unsecured financing is not backed by the assets or machinery of your company. In case you can’t pay back the whole loan, a secured loan will ask for your property as “security.” Products for business credit might be secured or unsecured. Secured loans employ the assets of your company as security; unsecured loans are independent of those assets. Many business loans are unsecured, but if the loan is large or there is a higher risk involved, security may be required.

Security is typically important for expensive machinery, structures, cars, and other items. If your business was unable to pay back the loan, the security would be removed to cover the debt.

monetary examples

- Unsecured loans are available through a wide range of banks and lending institutions, including Funding Circle, Barclays, NatWest, and others.

- Secured loans: These loans, which often start at £25,000 or more, are offered by many of the same funding sources.

#15. Short-term loans

Short-term loans are an alternative to typical bank or credit union business loans that you may apply for online. Even though term loans and STLs are occasionally combined, an STL has several distinctive qualities. Which are:

- Instead of using interest rates, factor rate fee structures

- Your daily cash flow is more important to the lender than your credit score.

- increased speed of financing (one to two days).

- greater overall loan cost (typically between 10% and 60% of the borrowing amount)

- increased frequency of repayment (often daily).

#16. Crowdfunding

Some firms can raise money online from their peers by using crowdfunding. Crowdfunding comes in four flavours: debt, reward, equity, and charitable. With rewards crowdfunding, you agree to offer your backers something in exchange for their contribution rather than having to pay the money back. Someone participates in your business through equity-based crowdfunding in exchange for a portion of your business or goods. You may also be required to pay a charge to the crowdfunding website.

#17. Business Grants

website: https://www.british-business-bank.co.uk/finance-hub/grants-finance/

The most challenging sort of business finance to obtain is business grants, sometimes known as “free money,” but if you believe you could be qualified, you should research your small business grant alternatives. Even though some NGOs and even privately-owned companies also provide small business grants, the majority of business awards are sponsored by the government (at the federal, state, or municipal levels).

Veterans can receive business grants from several organisations, and there are many business awards specifically for women. Innovative digital businesses may qualify for grants from the government-supported Small Business Innovation Research (SBIR) programme worth up to $1.5 million. If you match the requirements, you may also apply for a Merchant Maverick’s Opportunity Grant.

How to get a Small Business Loan in the UK

The British Business Bank created the government-backed Enterprise Finance Guarantee (EFG) to support the expansion of small enterprises by securing loans between £25,000 and £1.2 million. You must be headquartered in the UK and have annual revenue of less than £41 million in order to qualify.

- NatWest Small Business Loan: is one of several flexible loans that NatWest provides, with durations up to 10 years. You may be able to borrow up to £50,000, but you might also need to put up security or a guarantee in order to do so.

- The HSBC Small Business Loan: HSBC provides a range of financing alternatives for loans between £1,000 and $25,000. At the beginning of the contract period, the bank provides a fixed interest rate and a three-month repayment holiday. Your repayments might be spread out over a period of between 12 months and 10 years.

- Royal Bank of ScotlandSmall Business Loan: With RBS’s adaptable small business finance choices, you may borrow anything between $1,000 and $50,000. You may pick a payback period from one to ten years, and the interest rate is set.

- Lloyds Business Loans: At Lloyds Bank, pick from a variety of funding choices. Between £1000 and £25,000 can be borrowed with fixed or variable interest rates for durations of up to 25 years. Also, Lloyds gives loans of more than £25,000 to businesses that make up to £25 million a year.

- Business loans from Funding Circle are available to businesses that don’t wish to pledge their assets as collateral. You may borrow anything between £50,000 and £500,000, but you must have been in business for at least three years. Additionally, there are no upfront costs or first-year payback obligations.

- The Greater London Investment Fund Loan (GLIF): If your organization is located in the capital of the UK, you may be eligible for a loan from the Greater London Investment Fund (GLIF), which might provide you with cash of between $100,000 and $1 million. You must have a strong business plan, and the loan will only be granted if you are unable to obtain financing from the private sector. SMEs without collateral or with a poor track record should consider the GLIF.

- Fredericks Foundation Loans: The Fredericks Foundation assists business owners who have struggled to find alternative sources of funding. Depending on your credit score and how long you’ve been in business, you could be eligible to borrow between £2,500 and £15,000 if you’ve been operating for less than 24 months. The foundation provides funding of up to £35,000 for SMEs older than two years.

")