Credit Karma guarantees that you will receive your accurate credit point total and credit report for free. So how accurate and trustworthy is this data? Is Credit Karma providing you with the exact knowledge that a lender would have if you applied for a personal loan or a car loan? Is it providing you with almost anything you can’t get anyway?

To begin, you should understand what Credit Karma is and what it does, as well as how its VantageScore differentiates from the more familiar FICO score.

Focus Points are as followed:

- In exchange for data about your purchasing behavior, It provides you with a free financial score and credit report. It then charges businesses to serve you personalized advertisements.

- Two of the three major credit bureaus, TransUnion and Equifax, give Credit Karma the scores and credit report information.

- Based on that data, It generates its own accurate VantageScore.

- Your Credit Karma score should be comparable to or close to your FICO score, which is likely to be checked by any prospective lender.

- The verity of your credit score, like “decent” or “super good,” is more important than the exact number, which can be different from source to source and changes often.

What exactly is Credit Karma?

Credit Karma is most well-known for providing users with free credit for their creditworthiness and reports. On the other hand, it markets itself as a website that provides its users with “the chance to create a better economic prospect.”

You are required to provide Credit Karma with some basic personal information in order to use the service. Typically, this information consists of nothing more than your name and the last four digits of your Social Security card number. After receiving authorization from you,It will access your credit reports, generate a VantageScore for you, and make it accessible to you. Credit Karma’s payment history ranges from 300 to 850, with 850 being the highest possible score.

Their credit ratings can be classified as one of the following three categories:

- Poor: between 300 and the low 600s

- Up to acceptable: Low to mid-600s to the middle 700s

- Excellent in addition to being exceptional in quality: Above mid-700s.

Is Credit Karma Accurate?

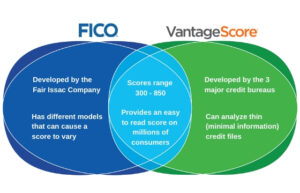

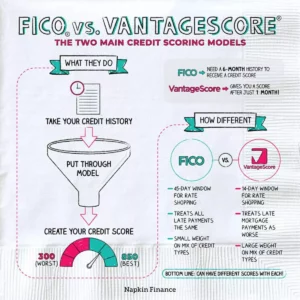

Even though the FICO score is widely considered to be the most recognizable credit score (and the one that almost every expert in the field of personal finance will tell you to keep an eye on), many individuals are unaware of the fact that FICO does not actually collect any information. The Fair Isaac Company, also known as FICO, is a model that is used to generate a score by looking at your files at the three major credit reporting bureaus.

The VantageScore offered a process followed by credit score that is very similar to the one described above, with the exception that its scoring model was actually developed by the credit bureaus. VantageScore claims to have scored 30 million more people than any other model, despite the fact that it is less well known to the general public.

One of the benefits of this method is that it can assign a score to individuals who have a limited credit history, also known as having a “thin” credit file. This might be a significant consideration for you if you are a young person or if you just moved to the United States recently.

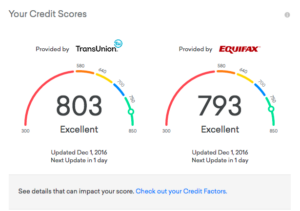

Credit Karma is not a credit bureau, which means that it does not collect information about its customers from their creditors. TransUnion and Equifax are two of the most important consumer credit bureaus. The credit scores and reports that you see on it reflect the information about your credit that has been reported to TransUnion and Equifax. Because these scores are not approximations of your accurate credit rating, you can rely on their accuracy and dependability.

The credit scores and reports that are displayed on Credit Karma are procured directly from two of the three major consumer credit bureaus, namely TransUnion and Equifax. The credit scores and reports that are displayed to you on it should accurately reflect the information about your credit that has been reported to the respective credit bureaus.

Scores on Credit Karma and Vantage

Business insiders reached out to Credit Karma to inquire as to the reasons why customers should have faith in the company’s ability to supply them with a score that is a reliable indicator of their credit standing.

Former Chief Consumer Advocate at Credit Karma Bethy Hardeman provided the following response: “The goals scored and borrowing questionnaires will be analyzed and will originally came from Allstate and Brokerage firms, two of something like the credit reporting agencies.”

“Independent of both major credit bureaus, we provide credit scores based on the VantageScore model. VantageScore was selected as the scoring model to be used by Credit Karma because it is a collaborative effort between the three major credit bureaus, it is a translucent ranking prototype, and it can assist consumers in better understanding changes that occur to their credit score.

Also Check: 17 Types of Business Loan For Small Businesses In 2022

Does It Really Matter Whether You Use Vantage Score or FICO?

Not to be confused with the FICO score. The name “FICO” refers to the Fair Isaac Corporation, which is the most formidable rival in the market for the production of scoring models that are employed to evaluate the creditworthiness of customers.

Both companies occasionally release updated versions of their models, and different lenders use slightly different versions of those models, which further complicates matters. Your score ought to be approximately the same regardless of which model you use. There is a possibility that one model places a marginally greater emphasis on outstanding medical bills.

The process of recording a loan application could take more time. However, if one system rates your credit as “good” or “very good,” then it ought to be identical to the other.

Vantage Score and FICO can both be examples of software programs that can determine a consumer’s credit rating by analyzing their expenditure and financial history. The FICO model is the more established option, having been first presented to the public in 1989.

Experian, Equifax, and TransUnion, the three most prominent consumer credit agencies, collaborated in the development of VantageScore, which was made available to the public in 2006.

Your FICO score and your VantageScore will invariably vary slightly from one another due to the fact that they are derived from two distinct scoring models. For said substance, you may receive a distinct FICO score at any given time from various sources, relying on whether the reference uses a specialized wide range of FICO or the most regularly used appearance package, and which of the model’s many versions is used. This can happen at any given time.

The most important thing to keep in mind is whether your points tally ought to be within the identical spectrum on each and every one of those models. It is not appropriate for you to possess an “excellent” VantageScore while your FICO score is only “equitable.”

Discrepancies Between FICO and Vantage Scores That Are Important to Know

The distinctions between a person’s FICO score and their Vantage Score are not all that significant:

The distinctions between a person’s FICO score and their Vantage Score are not all that significant:

- The purpose of VantageScore is to monitor individuals who use credit infrequently or for the first time. This could be an additional benefit for emerging adults, as well as anyone else who, for whatever reason, has fallen off the radar of consumers for a period of time.

- Your credit score will be checked whenever you request a new loan with a mortgage lender. It is a requirement of consumer protection law that multiple applications be treated like one query. This ensures that you are not penalized multiple times for shopping around and comparing prices.

- Due to the fact that the two competitors approach these queries in slightly different ways, it is possible that

- VantageScore will penalize you slightly further than FICO will.

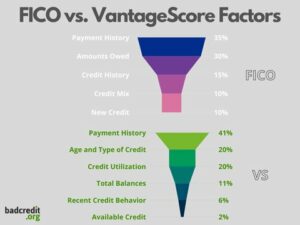

- Both will generate creditworthiness at the exact moment that it is required. The current information that is disclosed to the reporting agencies is the primary source of data used by the FICO system.

- The VantageScore model takes into account information on how you’ve managed your finances financially over the preceding two years.

Resemblances between FICO and Vantage scores

FICO and VantageScore are two different scoring models, but they both aim to achieve the same simple objective: to determine how likely it is that a consumer will be unable to pay back debt within the next two years.

FICO and VantageScore are two different scoring models, but they both aim to achieve the same simple objective: to determine how likely it is that a consumer will be unable to pay back debt within the next two years.

- Because of this, you shouldn’t let yourself become unduly concerned about the differences. If you have multiple credit scores, they should all be within a similar ballpark estimate, but they will never be exactly the same.

- Lending institutions utilize subscores. It is possible that it does not make a difference whether you rely on your FICO score or your VantageScore because you cannot forecast whether the scoring rate they will choose. There are a lot of other scoring models, and there is no sensible way that you could stay on top of them all or connect directly to them all at once.

Additional Services That Credit Karma Provides

Credit Karma will retrieve information about your credit history from one of the two large consumer credit agencies—namely, TransUnion and Equifax. (Experian is the third option.) It will generate its own unique self-governing rating based on the VantageScore system. After that, you will be provided with your prevailing VantageScore rating in addition to the more in-depth credit reports that support it.

It provides additional services that are related to this free service. These additional services include a security tracking service as well as alerts that notify you when somebody has performed a credit analysis on you.

This is not something that is exclusive to Credit Karma; a large number of strong credit status monitoring offer alerts and services that are very similar to these.

It will provide you personal information, you will be able to search for personalized offers for a credit card, a car payment, or a home loan. Your search will not appear in your credit score on Credit Karma or anywhere else, and it won’t show up anywhere else, either. “Inquiries” is a standard section that is included in credit reports. It lists the queries for your document that lenders who have received your loan application have made. You have the ability to restrict the number of queries you make using Credit Karma.

It also provides customers with individualized recommendations on how to better manage their finances. Example: “The rate on your auto loan is 16%. It’s possible that you’re paying too much!

How Credit Karma Generates Its Revenue

The Credit karma marketing strategy behind Karma is not one that is driven solely by altruism. It’s a profit-making company that generates money by paying enterprises to serve targeted ads to its customers in exchange for providing those clients with complimentary credit scores in exchange for additional information regarding their spending behaviors.

Credit Karma puts banner ads in the path of its consumers with the expectation that those users will interact with the advertisements by simply clicking on them. It may receive compensation if you apply for a loan through one of its links, given that many of these marketers are financial institutions.

Your personally identifiable information is valuable to advertisers, and as a result, they are willing to shell out more to target it and boast more than one hundred million active users.

Credit Karma FAQs

The Downsides of Credit Karma

Your first consideration should be whether or not you require the paid or free services that Credit Karma provides. And this may be contingent on how quickly you require specific information regarding the status of your credit. Remember:

Once every twelve months, you have the legal right to request a duplicate of your credit history as well as your credit history from each one of the three bureaus.

The majority of financial institutions, including banks and lenders, provide customers including on access to their creditworthiness. If you own an American Express card, for instance, you can view both your current FICO score and your FICO history by clicking on the Account Services tab.

That’s adequate for the vast majority of us, the vast majority of the time. If you are in the process of applying for a mortgage, attempting to boost your creditworthiness, or are interested in the related services that will provides you may find that having access to financial surveys and to the linked products that the company provides is beneficial to you.

It’s Possible That Your Credit Karma Score Is Not High Enough

On Credit Karma, it’s completely possible for your credit ratings to shift on a daily basis. The answer is largely contingent on the frequency with which your financial institutions investigate the financial institution. Now it provides the ability to check your daily credit score obtained from TransUnion.

Even though the VantageScore framework is precise, it is not the standard used in the industry. Its functions adequately for the typical customer, but the businesses that will decide whether or not to accept your request are much more likely to think about your FICO score.

Credit Karma Will Encourage Borrowing

Karma’s business model consists of earning revenue through advertising as well as commissions from loans that are obtained through the site. Despite the fact that the website presents itself as a reliable advisor, its primary goal is to get you to sign up for new loans.

Instead of using Credit Karma to get counsel on whether or not you should take on additional debt, use it to monitor your score.

Is it truly free to use Credit Karma?

Yes. It will not assess any fees for your use of their service. You will be required to pay a fee to the business in order to submit an application for a loan through the website.

Who is Responsible for Credit Karma?

Credit Kenneth Lin, Ryan Graciano, and Nichole Mustard launched the multi-national corporation known as Karma in the year 2007.

At the present time, Lin holds the position of chief executive officer, Graciano holds the position of chief operating officer, and Mustard holds the position of a chief revenue officer.

Intuit, the company that is responsible for TurboTax, successfully completed the acquisition of Credit Karma in December of 2020 for a total price of approximately $4.7 billion, which also included approximately $3.4 billion in cash along with 13.3 million shares of Intuit stock and equity awards.

Summary

Credit Karma helps millions track their credit scores. Vantage Score provides the company’s services. Thus, it shows your current credit status. It can spot credit report errors. As Hardeman advises, “monitor your credit regularly to catch inaccuracies or fraud.” Before applying for credit, dispute inaccuracies.

There are free alternatives to Credit Karma. Credit card companies and banks may offer online updates. You can get a free copy of your credit file annually at Annual CreditReport.com. It helps with loan research. A facility that provides a recent credit score instead current credit offers can be helpful if you’re looking for a loan. Credit Karma relies on these offers. Its advertisers want to loan you money, which could hurt your credit.